I get this question a lot. Why insurance? Of all the industries you could have started a company in, why the one famous for fine print, pushy salesmen, and fighting every claim? The one where the running joke is that the only thing slower than getting a payout is the industry itself adopting anything new?

Fair questions. I had some of the same stereotypes going in. But after spending real time inside this industry, I've come to believe that almost everything people think they know about insurance is wrong. Or at least, incomplete.

Let me explain.

The OG of Big Data

Before there was Big Data, before there were computers, before there were even punch cards or calculators.. the gentlemen at Lloyd's of London were writing probabilities in registers. Probabilities of weather. Probabilities of mortality. Probabilities of a ship making it back from the East India Company routes.

Insurance has always been a game of data. It's just that nobody talks about it that way.

On one side, it's all structured data. Numbers, math, actuarial formulas. On the other side, it's all contracts. Binding, consequential, deeply complex contracts. And that combination is what makes it fascinating.

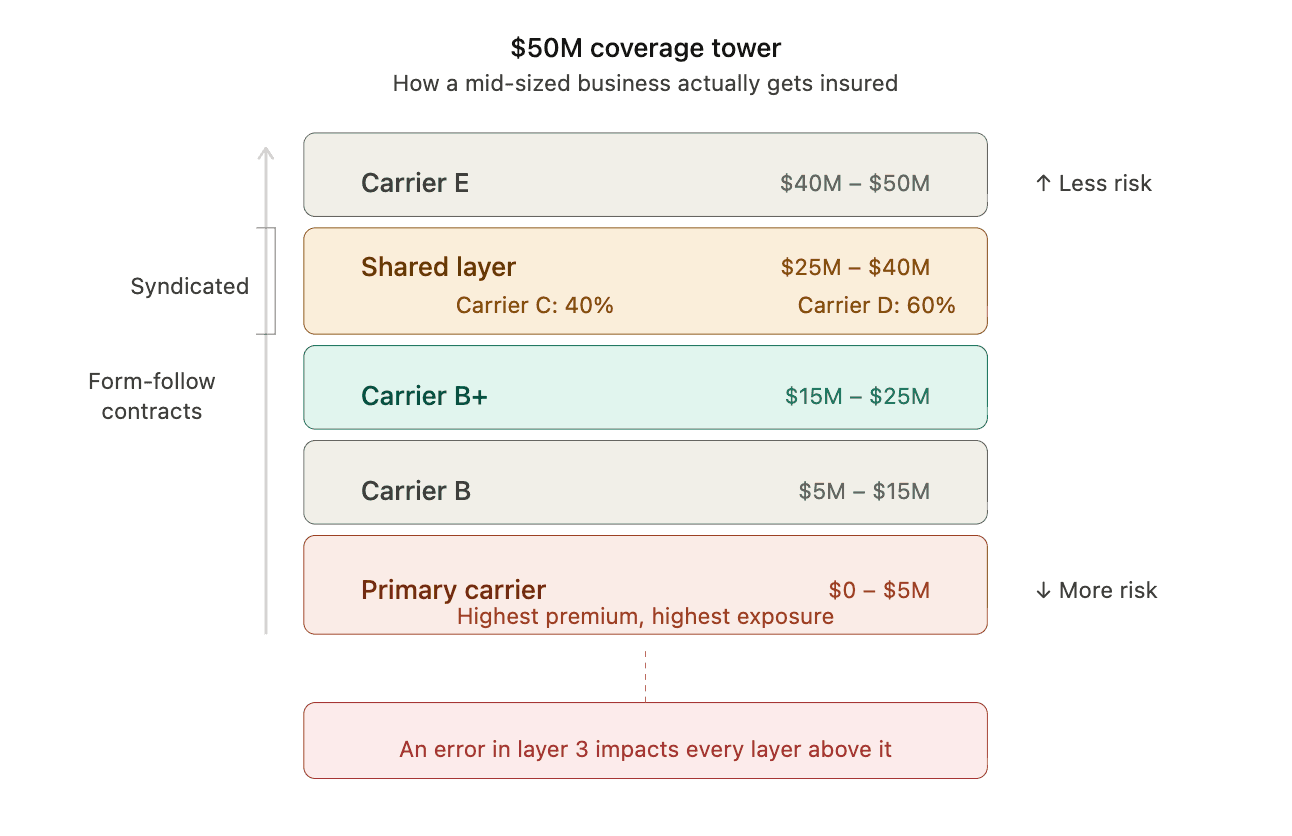

Think about how a large business gets insured. A company might need $50 million in coverage. No single carrier might be willing to take that on alone. So what happens? An agent assembles a tower, layered coverage across multiple carriers. The first carrier covers the first $5 million and takes the highest premium because they have the most exposure. The next covers $5 to $15 million for a lower premium. And somewhere in the upper layers, you might have two or three carriers sharing a single tranche horizontally in a 40/60 or 30/30/40 split.

Commercial Insurance is Complex!

It's a syndication. And every layer is governed by form-follow contracts, meaning the language of the first contract is binding on every contract above it. Now imagine someone in the third layer makes an error. A fat finger, a momentary distraction, lack of knowledge and understanding or just a complexity or nuance easy to miss even for an expert. Everything above that layer is impacted.

And nobody finds out until a lawsuit triggers the policy!

Time Bombs in Fine Print

These errors, called E&O (errors and omissions), are not edge cases. They're built into the financial model. Agencies budget 2-3% of revenue for the lawsuits and reimbursements that come from mistakes that slipped through. And those are just the ones that get exposed because a bad outcome actually happened. There are plenty more buried errors sitting quietly in policies that have never been invoked.

Time bombs, basically.

Or think about this. You're signing a new contract and your client needs a certificate of insurance to get the deal done. There's pressure, there's a deadline, and you go to your agent and insist they issue the certificate with the language needed to close. Neither you nor the agent, under that pressure, have the time to think through whether the hurriedly written language on that certificate would come back and bite you when something actually goes wrong. And when it does, there's nothing you can do about it.

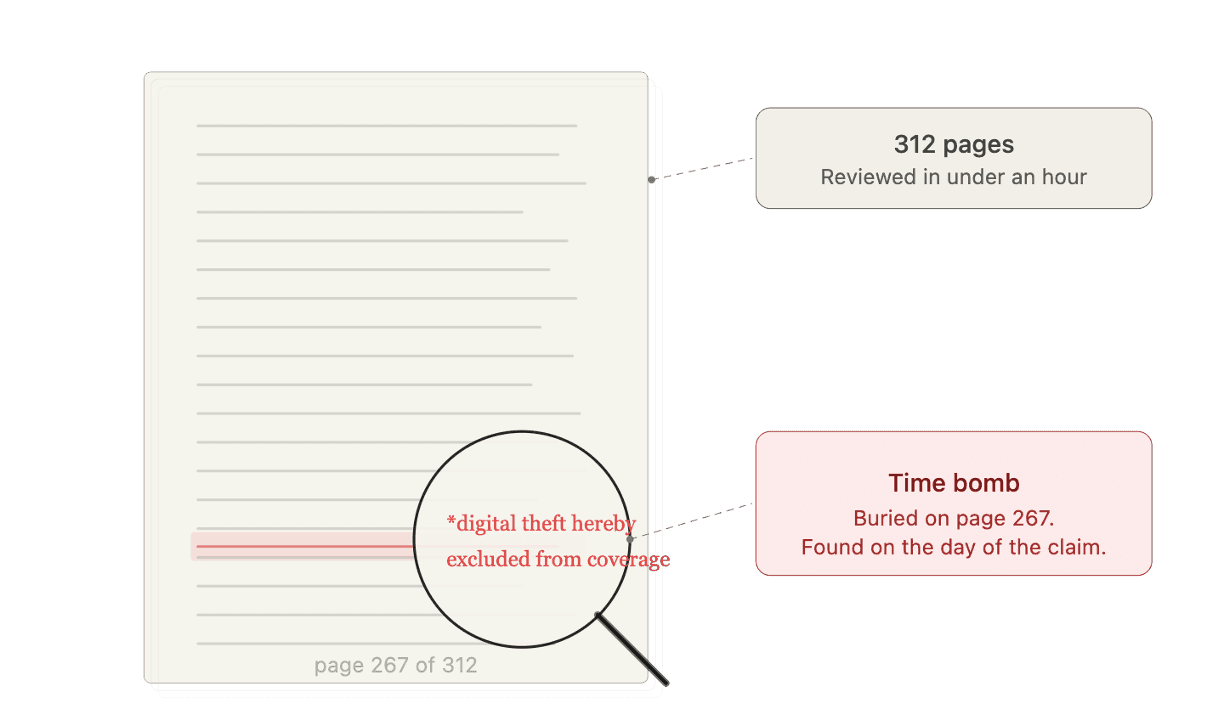

And it goes deeper than the commercial side. Your homeowner's renewal comes in, and somewhere on page 42 there's a line that says digital theft is now excluded, or roof damage above a certain threshold is no longer covered. Most people will never catch that. They'll just wonder why their premium went up.

Buried Time Bombs hidden in plain sight

The Fabric Underneath American Prosperity

Here's something most people don't fully appreciate: insurance is what keeps the rest of the economy functioning. If insurance didn't exist, lawyers wouldn't exist, because who do lawyers sue? They sue companies with deep pockets, and if they did not protect themselves, they would harm the entire business. Any business is fundamentally full of uncertainties, and there are many things that could go wrong, and its important for the business owners, shareholders the employees and the customers to be protected. But it should not mean that you spend all your mind and energy on risk mitigation. Even so, a huge portion of corporate legal work today is actually just making sure insurance policies are airtight.

And for smaller businesses that can't afford legal teams? Their insurance agent is their advisor. Carrying an enormous amount of responsibility with no law degree. The expertise to do that job well only comes from years of grinding through contracts on the ground.

So about that stereotype of the pushy insurance salesman? The reality is that most agents are doing incredibly nuanced, high stakes work. They're assembling complex coverage structures, advising businesses on risk, and reading through contracts that can range from 20 pages to sometimes thousands of pages, full of sophisticated exclusions, conditions, and interdependencies. The ones who are good at this are genuinely protecting not just people and their homes and assets, but entire businesses and the livelihoods that come out of them.

American Exceptionalism and Progress Supported By the Insurance Framework

Slow Was Not the Industry. Slow Was the Tech.

Insurance gets criticized for being slow to adopt technology. Resistant to change. Stuck in their ways. I used to hear that too, and it sounded reasonable from the outside.

But when you get inside, you realize the truth is completely different.

The hardest problems in this industry have always been two things: doing complicated math across enormous datasets, and doing very deep analysis of painfully complex content. Contracts that are 20 pages on a good day and thousands of pages on a bad one, with layered structures, form-follow dependencies, exclusions buried inside exclusions, and every single word carrying legal weight.

And what did technology offer them?? Data entry tools.

That's it. Tech didn't help them do any of their actual work. Instead, it insisted that whatever work they did, they spend more time keeping a record of it in the computer. Here, fill out these mundane forms. Navigate these clunky portals. Enter this data into this system so it can live in that system. Oh, and by the way, we're not going to help you analyze a single page of that 300 page contract you're reviewing tonight.

No wonder the industry was skeptical. They weren't slow to change. The tech just wasn't giving them anything worth changing for.

Legacy tech hurts more than it helps

Having spent my career in machine learning, text mining, and large scale data systems, I knew the moment I got deep into this industry that all of this was about to change. We were standing at the cusp of generative AI, neural networks, and deep learning, technologies that could finally tackle the two hardest problems insurance professionals face every single day. The math and the contracts. The numbers and the words. All of it, at a quality level that not only matches but more recently far exceeds what humans can do.

So we took the leap of faith. And boy, has it been a great decision!

The People

Working in this industry, I've had the chance to interact with insurance agents, brokers, distributors, underwriters, often generational companies that have thrived on the simple but powerful concept of building relationships with their clients. And I have come out deeply impressed.

This journey has gotten me out of my San Francisco and New York tech bubble and into the heart of America, where insurance actually lives. I have found mentors in this industry, friends in this industry, advisors in this industry. And I have been humbled by how warmly they have welcomed us outsiders, how generously they have shared their knowledge, and how much trust and encouragement they have given us. It makes my day, week, month and year when a producer or agency owner who has been doing this for 40 years comes and tells us, "Thank you Anshu and Vishal, for making Outmarket."

I carry a deep sense of respect for the insurance professionals who have been doing the work of lawyers without a law degree, the work of data scientists without a computer science degree, and the work of financial advisors without a Wall Street pedigree. These are people who have quietly held together the risk fabric of this country through sheer grit, relationships, and hard earned expertise, by printing hundreds of pages of policy documents and poring over them day in and day out.

An industry built on people and their relationships

The insurance industry sits on 300 years of data and contracts. The tools to actually make sense of all of it at scale are just now arriving. The industry is ready. The people are ready. And they're adopting AI in their daily work faster than many programmers I know. So.. that's why me and Vishal Sankhla started Outmarket AI!

I get this question a lot. Why insurance? Of all the industries you could have started a company in, why the one famous for fine print, pushy salesmen, and fighting every claim? The one where the running joke is that the only thing slower than getting a payout is the industry itself adopting anything new?

Fair questions. I had some of the same stereotypes going in. But after spending real time inside this industry, I've come to believe that almost everything people think they know about insurance is wrong. Or at least, incomplete.

Let me explain.

The OG of Big Data

Before there was Big Data, before there were computers, before there were even punch cards or calculators.. the gentlemen at Lloyd's of London were writing probabilities in registers. Probabilities of weather. Probabilities of mortality. Probabilities of a ship making it back from the East India Company routes.

Insurance has always been a game of data. It's just that nobody talks about it that way.

On one side, it's all structured data. Numbers, math, actuarial formulas. On the other side, it's all contracts. Binding, consequential, deeply complex contracts. And that combination is what makes it fascinating.

Think about how a large business gets insured. A company might need $50 million in coverage. No single carrier might be willing to take that on alone. So what happens? An agent assembles a tower, layered coverage across multiple carriers. The first carrier covers the first $5 million and takes the highest premium because they have the most exposure. The next covers $5 to $15 million for a lower premium. And somewhere in the upper layers, you might have two or three carriers sharing a single tranche horizontally in a 40/60 or 30/30/40 split.

Commercial Insurance is Complex!

It's a syndication. And every layer is governed by form-follow contracts, meaning the language of the first contract is binding on every contract above it. Now imagine someone in the third layer makes an error. A fat finger, a momentary distraction, lack of knowledge and understanding or just a complexity or nuance easy to miss even for an expert. Everything above that layer is impacted.

And nobody finds out until a lawsuit triggers the policy!

Time Bombs in Fine Print

These errors, called E&O (errors and omissions), are not edge cases. They're built into the financial model. Agencies budget 2-3% of revenue for the lawsuits and reimbursements that come from mistakes that slipped through. And those are just the ones that get exposed because a bad outcome actually happened. There are plenty more buried errors sitting quietly in policies that have never been invoked.

Time bombs, basically.

Or think about this. You're signing a new contract and your client needs a certificate of insurance to get the deal done. There's pressure, there's a deadline, and you go to your agent and insist they issue the certificate with the language needed to close. Neither you nor the agent, under that pressure, have the time to think through whether the hurriedly written language on that certificate would come back and bite you when something actually goes wrong. And when it does, there's nothing you can do about it.

And it goes deeper than the commercial side. Your homeowner's renewal comes in, and somewhere on page 42 there's a line that says digital theft is now excluded, or roof damage above a certain threshold is no longer covered. Most people will never catch that. They'll just wonder why their premium went up.

Buried Time Bombs hidden in plain sight

The Fabric Underneath American Prosperity

Here's something most people don't fully appreciate: insurance is what keeps the rest of the economy functioning. If insurance didn't exist, lawyers wouldn't exist, because who do lawyers sue? They sue companies with deep pockets, and if they did not protect themselves, they would harm the entire business. Any business is fundamentally full of uncertainties, and there are many things that could go wrong, and its important for the business owners, shareholders the employees and the customers to be protected. But it should not mean that you spend all your mind and energy on risk mitigation. Even so, a huge portion of corporate legal work today is actually just making sure insurance policies are airtight.

And for smaller businesses that can't afford legal teams? Their insurance agent is their advisor. Carrying an enormous amount of responsibility with no law degree. The expertise to do that job well only comes from years of grinding through contracts on the ground.

So about that stereotype of the pushy insurance salesman? The reality is that most agents are doing incredibly nuanced, high stakes work. They're assembling complex coverage structures, advising businesses on risk, and reading through contracts that can range from 20 pages to sometimes thousands of pages, full of sophisticated exclusions, conditions, and interdependencies. The ones who are good at this are genuinely protecting not just people and their homes and assets, but entire businesses and the livelihoods that come out of them.

American Exceptionalism and Progress Supported By the Insurance Framework

Slow Was Not the Industry. Slow Was the Tech.

Insurance gets criticized for being slow to adopt technology. Resistant to change. Stuck in their ways. I used to hear that too, and it sounded reasonable from the outside.

But when you get inside, you realize the truth is completely different.

The hardest problems in this industry have always been two things: doing complicated math across enormous datasets, and doing very deep analysis of painfully complex content. Contracts that are 20 pages on a good day and thousands of pages on a bad one, with layered structures, form-follow dependencies, exclusions buried inside exclusions, and every single word carrying legal weight.

And what did technology offer them?? Data entry tools.

That's it. Tech didn't help them do any of their actual work. Instead, it insisted that whatever work they did, they spend more time keeping a record of it in the computer. Here, fill out these mundane forms. Navigate these clunky portals. Enter this data into this system so it can live in that system. Oh, and by the way, we're not going to help you analyze a single page of that 300 page contract you're reviewing tonight.

No wonder the industry was skeptical. They weren't slow to change. The tech just wasn't giving them anything worth changing for.

Legacy tech hurts more than it helps

Having spent my career in machine learning, text mining, and large scale data systems, I knew the moment I got deep into this industry that all of this was about to change. We were standing at the cusp of generative AI, neural networks, and deep learning, technologies that could finally tackle the two hardest problems insurance professionals face every single day. The math and the contracts. The numbers and the words. All of it, at a quality level that not only matches but more recently far exceeds what humans can do.

So we took the leap of faith. And boy, has it been a great decision!

The People

Working in this industry, I've had the chance to interact with insurance agents, brokers, distributors, underwriters, often generational companies that have thrived on the simple but powerful concept of building relationships with their clients. And I have come out deeply impressed.

This journey has gotten me out of my San Francisco and New York tech bubble and into the heart of America, where insurance actually lives. I have found mentors in this industry, friends in this industry, advisors in this industry. And I have been humbled by how warmly they have welcomed us outsiders, how generously they have shared their knowledge, and how much trust and encouragement they have given us. It makes my day, week, month and year when a producer or agency owner who has been doing this for 40 years comes and tells us, "Thank you Anshu and Vishal, for making Outmarket."

I carry a deep sense of respect for the insurance professionals who have been doing the work of lawyers without a law degree, the work of data scientists without a computer science degree, and the work of financial advisors without a Wall Street pedigree. These are people who have quietly held together the risk fabric of this country through sheer grit, relationships, and hard earned expertise, by printing hundreds of pages of policy documents and poring over them day in and day out.

An industry built on people and their relationships

The insurance industry sits on 300 years of data and contracts. The tools to actually make sense of all of it at scale are just now arriving. The industry is ready. The people are ready. And they're adopting AI in their daily work faster than many programmers I know. So.. that's why me and Vishal Sankhla started Outmarket AI!

Ready to Transform Your Agency?

Ready to Transform Your Agency?

Ready to Transform Your Agency?

The #1 AI platform for insurance. 250+ agencies. Purpose-built workflows. Enterprise security.

The #1 AI platform for insurance. 250+ agencies. Purpose-built workflows. Enterprise security.

The #1 AI platform for insurance. 250+ agencies. Purpose-built workflows. Enterprise security.

Platform